A lot of people first learn the phrase work credits from a denial letter.

Wondering what your claim could be worth? Try our free SSDI benefits calculator.

They're in their late 50s or early 60s. Their back is gone after years of lifting. Their knees won't tolerate standing all day. A heart condition, cancer treatment, neck problems, or a neurological disease has pushed them out of work. They apply for SSDI because they believe, reasonably, that they've paid into Social Security for decades. Then the letter says they aren't insured, or that they don't have enough recent work credits.

That feels wrong because, in a common-sense way, it is wrong to the person living it. You've worked. You've paid taxes. You've done your part. But Social Security doesn't use common-sense shorthand on this issue. It uses a technical insurance rule. If you don't understand that rule, it's easy to miss a problem until after a denial.

You've Worked Your Whole Life Now What Are Work Credits

A typical claimant in this age group doesn't come in asking abstract questions about Social Security policy. They come in because their degenerative disc disease, shoulder injury, failed knee replacement, neuropathy, heart problem, or cancer has made regular work unrealistic, and the SSDI process suddenly turns on a phrase they've never needed before.

The confusion usually sounds like this: "I worked for years. How can they say I don't qualify?"

The answer is that Social Security disability has a medical side and a technical side. The medical side asks whether your condition keeps you from substantial work. The technical side asks whether you're still insured for SSDI at the time your disability began. Work credits are the units Social Security uses to answer that second question.

For people between 50 and 64, this issue can be especially frustrating. Many have a long work history, but also a stretch of reduced work before filing. That gap might come from worsening pain, surgeries, caregiving, layoffs, or trying to push through a physical condition with part-time work until the body finally says no.

Denied? You have only 60 days to appeal.

Talk to a disability attorney now. Free consultation. No fees unless you win.

Call (617) 683-1983Many people don't lose SSDI because they weren't sick enough. They lose because the record didn't show enough recent insured status when they stopped being able to work.

That doesn't mean the situation is hopeless. It means the timing of your disability, your earnings record, and the kind of work you did matter more than is commonly understood. If you've been denied or you're worried about your coverage, the first step isn't guessing. It's understanding exactly what Social Security counts, what it doesn't, and where your record may need a closer look.

Understanding Work Credits as Your Insurance Premiums

The cleanest way to understand what are social security work credits is to think about them as insurance premiums.

When you worked and paid Social Security taxes through wages or self-employment income, you weren't just building toward retirement. You were also paying into a disability insurance system. Social Security calls the basic units work credits, also known as quarters of coverage. Those credits are the receipts showing you've paid into the system through covered work.

What credits do and what they don't do

Many applicants often misunderstand this aspect. Credits answer an eligibility question. They do not calculate your monthly benefit amount.

If Social Security were a locked door, work credits would be the key. They get you to the doorway. They don't decide what's inside the check.

Core rule: Work credits determine whether you can qualify for SSDI. They do not determine how much your monthly SSDI benefit will be.

That distinction matters because people often assume a long work history automatically fixes every issue. It doesn't. You can have many years of work and still run into a problem if your recent work history doesn't meet SSDI's insurance rules. On the other hand, piling up extra credits beyond what the system requires won't increase the monthly disability benefit by itself.

Why this matters for older workers with physical conditions

People in their 50s and early 60s often have exactly the kind of records that create confusion. They may have worked hard for decades in construction, nursing, warehouse work, driving, maintenance, manufacturing, food service, or other physically demanding jobs. Then their condition worsens, and the last few years become uneven. There may be lighter work, reduced hours, leave periods, or no work at all.

Social Security tracks credits because SSDI is insurance tied to covered work. The system asks, in effect, whether you were still insured when disability forced you out of the workforce. That is why the question isn't just "Did you ever work?" It's "Were you still covered when your disabling condition took you off the job?"

How Work Credits Are Earned and Calculated Each Year

Work credits are earned by dollars, not by effort, seniority, or time on the clock. A person can work only part of the year and still get all four credits. Another person can stay employed much longer, but come up short if earnings were too low or were not reported as covered wages.

In 2026, you earn one Social Security work credit for every $1,890 in covered earnings, and you can earn no more than four credits for the year. Once covered earnings reach $7,560, you have the full four credits for that year, according to the Social Security Administration's credit rules.

The simple math

The math is straightforward:

- One credit: Earn $1,890 in covered wages or self-employment income in 2026.

- Four credits for the year: Reach $7,560 in covered earnings in 2026.

- No extra credits after that: Higher earnings may affect benefit calculations later, but they do not produce more than four credits for that year.

I often have to clear up a common misunderstanding here. Social Security is not counting how hard you worked or how many months you pushed through pain. It is checking whether enough covered earnings were posted to your record in that calendar year.

A good way to picture it is a yearly punch card with only four spaces. Once all four spaces are filled, that year's credit question is over.

Hours don't control the result

Hours by themselves do not decide anything. Earnings do.

A worker who picks up a few strong months early in the year can earn all four credits quickly. A worker whose hours were reduced because of back problems, joint damage, heart symptoms, or recovery from surgery may stay attached to a job all year and still miss a credit if wages never reach the threshold. That distinction is especially important for workers between 50 and 64, because the last few working years are often uneven.

Not sure if you qualify?

Get a free case review from a New England disability team. You only pay if we win.

Call (617) 683-1983This comes up all the time with people who shifted to lighter duty, took intermittent leave, or tried to hang on in a smaller role before stopping work altogether. A year that felt incomplete may still count fully. A year that looked steady on paper may not.

A work credit is an earnings measure for a specific year.

The threshold changes over time

The amount needed for one credit changes from year to year. The verified figures show $1,640 per credit in 2023, $1,810 per credit in 2025, and $1,890 per credit in 2026, with the four-credit maximum reached at the matching yearly earnings amounts.

This detail is critical when reviewing an earnings record year by year. One year's threshold cannot be applied to every prior year.

For older workers with long careers, that review is where mistakes happen. Someone may assume, "I worked that year, so I must have my credits." Sometimes that is true. Sometimes a year included reduced wages, unpaid leave, failed self-employment income, or an employer reporting problem. If your condition worsened gradually and your work faded out instead of stopping all at once, each year near the end of your work history needs a careful look.

The Two Critical Tests for SSDI Eligibility After Age 50

A worker in his late 50s comes into my office after 35 years on the job. His back is shot, his knees are worse, and he assumes SSDI will at least be available because he has paid into the system for decades. Sometimes that is true. Sometimes the case stalls before Social Security even reaches the medical evidence.

SSDI uses two separate insurance tests. One asks whether you built up enough work over your lifetime. The other asks whether you worked recently enough before your disability began. For workers between 50 and 64, the second test is often the harder one.

The duration test and the recent work test

The duration test looks at your total work history. The recent work test looks at timing.

For workers age 31 or older, the general rule is familiar. Social Security usually expects a long enough earnings record to satisfy the lifetime requirement, and it also usually expects 20 credits in the 10 years before disability began. In plain English, that means about five years of covered work during the decade leading up to your onset date.

Here is the basic framework:

| Age disability begins | Work credits needed under the duration test | Recent work test details |

|---|---|---|

| Under 24 | Fewer credits may qualify | Need 6 credits in the 3-year period ending when disability begins |

| Ages 24 to 30 | Scaled requirement | Need credits for half the time between age 21 and disability onset |

| Age 31 and older | Generally a longer lifetime work record is required | Need 20 credits in the prior 10 years, which is about 5 years of work |

If you are reading this in your 50s or early 60s, the last row is usually the one that decides the case.

A practical comparison helps. The duration test asks, "Were you insured under this program at all?" The recent work test asks, "Were you still insured when your body stopped letting you work?" A long career helps with the first question. It does not always solve the second.

Why the recent work test causes trouble in your 50s and 60s

Physical conditions often wear people down in stages. A construction worker with spinal stenosis cuts back to lighter duty. A warehouse employee with shoulder damage starts missing shifts. A machine operator with heart disease tries part-time work, then burns through leave, then stops. By the time the claim is filed, the primary dispute may be whether disability started while insured status was still in place.

That is the trap for older workers. A person may have 25 or 30 strong years behind them and still run into a technical denial if the last several years were thin, interrupted, or outside covered employment.

The date your disability began is not just a medical detail. It can decide whether your recent credits still count for SSDI.

The onset date is therefore a critical detail in SSDI cases for older workers. If the medical record supports an earlier onset date, that date may fall inside the insured period. If the evidence points to a later date, Social Security may decide coverage had already run out before disability began.

I see this issue most often with people who tried to push through pain for too long. That effort is understandable. It can also complicate the claim.

What helps and what does not

What helps:

- Pinpointing when work became unsustainable. The key question is not when the condition first appeared. It is when it became severe enough to prevent substantial work.

- Reviewing earnings year by year. Older workers often have a mixed final stretch, with reduced hours, unpaid leave, or stop-and-start employment.

- Matching the medical timeline to the work-credit timeline. A strong diagnosis alone is not enough if the supported onset date falls after insured status expired.

What does not help:

- Relying only on the fact that you worked hard for decades.

- Assuming Social Security retirement rules and SSDI insurance rules are the same.

- Filing before confirming your date last insured and whether your recent earnings satisfy the rule.

For claimants ages 50 to 64, this is often the first hard gate in the case. If you do not meet both tests, Social Security never gets to the full medical analysis, no matter how serious the condition is.

Worried a misstep could cost you benefits?

A short, free consultation now can prevent an expensive mistake later. No upfront fees.

Call (617) 683-1983How Work Gaps Military Service and Self-Employment Affect Credits

A long work history can still leave a dangerous hole in an SSDI claim.

I see it often with workers in their 50s and early 60s. They spent decades on the job, then a back injury, heart condition, joint replacement, or cancer treatment disrupted the last few working years. On paper, Social Security is not measuring effort or loyalty to work. It is checking whether enough covered work appears in the right time period.

The first issue I would flag for claimants ages 50 to 64 is work gaps.

The hard part is that many of these gaps make perfect sense in real life. Someone stops working to recover from surgery. Someone cuts back to care for a spouse. Someone tries to return, lasts a few months, then has to stop again because standing, lifting, or keeping a schedule is no longer realistic. Those gaps may feel temporary to you, but they can interrupt the recent work record Social Security uses for SSDI.

As noted earlier, credits can stay on your record for years. The problem is timing. For older workers, the last stretch of employment often matters more than the fact that they worked steadily for most of adulthood. In practice, the question becomes whether disability began before insured status ran out.

Work gaps can break recent insured status

Work credits work like insurance premiums. Years ago, you paid in. SSDI asks whether that coverage was still active when you became unable to work.

That is why onset date matters so much for this age group. A claimant may have a strong medical case and a very long work history, yet still face a technical denial if the supported disability date falls after coverage expired. I have seen this happen with factory workers who kept pushing through shoulder damage, drivers who kept working through worsening neuropathy, and nurses who tried to hang on after repeated surgeries.

A gap does not automatically end the case. It does mean the timeline has to be built carefully, with medical records, earnings history, and the actual point where full-time work stopped being sustainable.

Self-employment only counts if the earnings made it onto the record

Self-employment creates a different problem. Many people with physical limitations try to piece together lighter work after leaving a more demanding job. They do ride-share driving, handyman jobs, consulting, resale work, delivery gigs, cleaning, or cash jobs because they are trying to keep money coming in.

Sometimes that effort helps. Sometimes it does not help at all for credits.

Social Security looks at covered earnings that were properly reported. If the income was not reported, or the net earnings were too low, the year may produce fewer credits than expected or none at all. That is an unpleasant surprise for claimants who believed any work activity would protect their insured status.

The practical trouble spots are usually these:

- Income was never reported correctly: Social Security may not count it if it does not appear on the earnings record.

- The work was real, but the earnings were too low: A person may have worked hard and still not earned enough in covered income for the available credits that year.

- Tax records were reviewed too late: People often discover the mismatch only after a denial or after seeing a date last insured they did not expect.

If you were self-employed, the central question is simple. Did Social Security receive and credit those earnings in a way that counts for SSDI?

Military service can help, but it does not fix every credit problem

Military service deserves a close review, especially for older claimants with long and varied work histories. Service earnings may strengthen the record. In some cases, they are part of why a claimant meets the overall duration requirement.

But veterans should not assume earlier service automatically solves a recent work problem. For many people between 50 and 64, military service sits far back in the timeline. It may support total coverage while doing little to cure a later gap between the last covered work and the disability onset date.

The practical step is verification. Review how the service period appears on the Social Security earnings record. Keep discharge paperwork and any other service records available in case Social Security raises a question.

These cases often turn on details that seem minor until they are not. A warehouse worker develops knee damage, leaves full-time work, then picks up sporadic 1099 jobs. A veteran with heart disease has years of solid prior work but a caregiving gap near the end. A construction worker with a neck fusion stops working, tries a few cash jobs, and assumes those months kept coverage alive. Each of those facts can change the credit analysis.

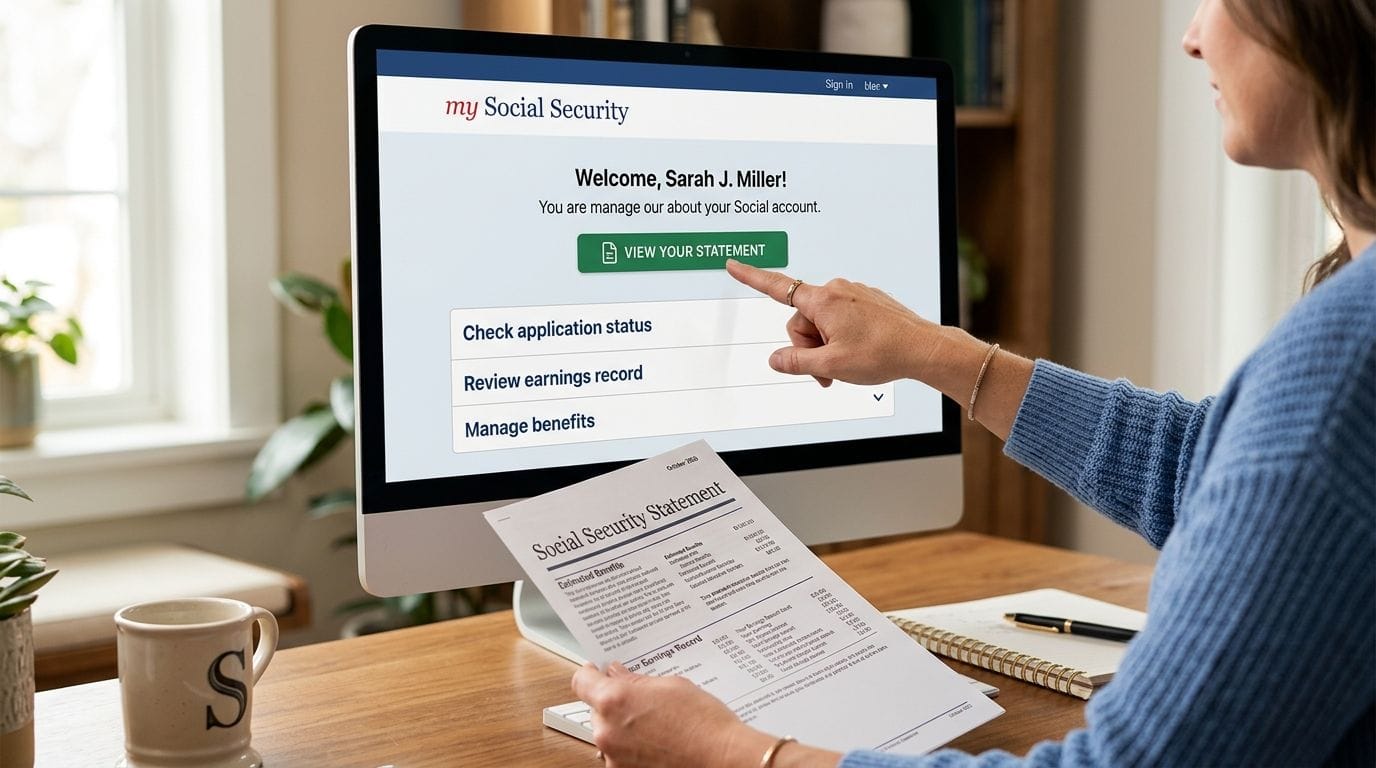

Finding Your Official Work Credit History

If you're worried about your SSDI coverage, the most useful thing you can do today is get your official earnings record from Social Security.

Want a straight answer about your claim?

Free consultation with an experienced SSDI team. No fees unless you win.

Call (617) 683-1983The practical tool for that is a my Social Security account. Once you create it through the SSA website, you can review your earnings history and see the record Social Security uses when it evaluates insured status and future benefits.

What to look for on the statement

Don't just glance at the total. Read it year by year.

You're looking for missing earnings, suspiciously low earnings, or years showing zero when you know you worked. This matters a lot for people whose last working years were uneven because of back problems, orthopedic injuries, heart conditions, or cancer treatment. The year you think "sort of counted" may not count the way you expect. Or the opposite may be true.

Check these items carefully:

- Year-by-year earnings: Compare the Social Security record to your own memory, W-2s, 1099s, or tax returns.

- Years near disability onset: These are often the most important years for the recent work test.

- Name and number consistency: If payroll records and Social Security records didn't match, earnings can be posted incorrectly or not at all.

Don't ignore errors

An earnings error can sink a claim if nobody catches it.

If you find a year that looks wrong, gather the documents that support the correction. That may include W-2s, tax returns, pay records, or proof of self-employment filings. Then follow Social Security's correction process promptly. Waiting rarely helps.

Your Social Security statement is not a rough estimate for SSDI purposes. It's the baseline record the agency uses unless you challenge an error with evidence.

A careful review is especially important if your work history includes part-time years, job changes, self-employment, or periods where illness cut your earnings down before you stopped completely. In claims for people ages 50 to 64, those edge years often decide whether the file moves forward medically or ends on a technical denial.

When to Call Melanson Law Group About Your SSDI Claim

If your denial letter mentions insured status, work credits, or a lack of recent coverage, that's usually the point to get legal help.

Work credits sound simple until you apply them to a real life. A long career with a late-stage physical breakdown. A gradual exit from work because of pain. A mix of payroll jobs and self-employment. Military service years. Missing earnings on the record. Those are exactly the situations where people make understandable mistakes, and where a technical review can change the direction of a case.

Good SSDI representation doesn't just argue that you're disabled. It also checks whether Social Security is using the right onset date, the right earnings history, and the right insured-status analysis. That's especially important for workers in their 50s and early 60s, because the medical rules may become more favorable with age, but only if the technical foundation is there.

If you're unsure whether you still have enough recent credits, if your work record is complicated, or if you've already been denied, this is the stage where careful legal review matters most.

If you're dealing with a denial, confused about your work credit status, or trying to prove disability after years of physically demanding work, Melanson Law Group can help you sort out the technical side of your SSDI claim and build the strongest case possible. The firm combines hands-on representation with the insight of retired Social Security judge Jack Melanson and works on a no-fee-unless-you-win basis.