If you're in your 50s or early 60s and your body has stopped cooperating, money worries usually arrive before the SSDI approval does. A bad back from degenerative disc disease, a failing knee after years of physical work, nerve damage, cancer treatment, heart problems, or chronic neck pain can push you out of the job market fast. Then the bills start stacking up. Hospital balances. Credit cards used to cover groceries. Car payments. Old tax notices. Collection letters that seem designed to raise your blood pressure.

Wondering what your claim could be worth? Try our free SSDI benefits calculator.

One of the most common questions people ask is simple and urgent. Can SSDI be garnished?

The short answer is that most private creditors cannot take your SSDI benefits, but there are important exceptions. That distinction matters. If you understand where the actual risks are, you can stop fearing every collection letter and start protecting the income you rely on each month.

Your SSDI Benefits Have a Federal Shield

A key reassuring rule for those receiving disability benefits is that Federal law protects SSDI from garnishment by private creditors. That means the common debts that pile up during a health crisis usually cannot reach your benefit payment itself.

Under the protection described here, private creditors such as credit card companies, personal loan lenders, and medical bill collectors cannot garnish SSDI benefits, and banks must automatically protect up to two months' worth of directly deposited SSDI benefits even if a private creditor gets a court judgment.

What that shield covers

For a claimant between 50 and 64, this is often the exact relief they need to hear. If you've been forced out of work by orthopedic problems, cancer, neurological disease, or heart trouble, the debts that usually follow are private debts.

That often includes:

- Medical bills: hospital balances, imaging charges, surgery bills, oncology treatment balances, rehabilitation invoices

- Credit cards: especially cards used to bridge the gap after work stopped

- Personal loans: loans taken out to cover rent, utilities, or family expenses

- Auto loans and other consumer debts: accounts tied to everyday life, not federal obligations

- Private student loans: not federal student loans, but private education debt

Those collectors may call. They may send letters. They may sue. What they generally can't do is take the SSDI payment itself.

Denied? You have only 60 days to appeal.

Talk to a disability attorney now. Free consultation. No fees unless you win.

Call (617) 683-1983Why this matters so much in your 50s and 60s

People in this age group often don't have time to rebuild from scratch. A person who spent decades doing warehouse work, construction, nursing assistance, machine operation, driving, or skilled trades may suddenly find that lifting, standing, walking, bending, or even sitting for long periods is no longer realistic.

When that happens, private debt tends to grow for practical reasons, not reckless ones. You use a card to pay for prescriptions. You finance travel to medical appointments. You cover household costs while waiting for a disability decision. The law recognizes that Social Security benefits are supposed to provide basic support, not serve as an easy target for ordinary collectors.

Practical rule: A threatening letter from a private collector isn't the same thing as legal access to your SSDI check.

That doesn't mean you should ignore lawsuits or court papers. It means you should separate noise from real exposure. A collection agency may sound powerful on the phone. Federal law is more powerful.

What this shield does not mean

This protection is strong, but it isn't a magic invisibility cloak. It doesn't erase the debt. It doesn't prevent a creditor from trying to collect in other lawful ways. And it doesn't mean every dollar in every account is automatically safe forever if funds are mixed together carelessly.

Think of SSDI protection like a fireproof box. If the benefit payment stays identifiable, the law gives it strong protection. If that money gets mixed with other deposits and left in an account without clear records, proving what should be protected can become harder.

A few practical points help:

- Keep records: save bank statements showing direct deposit from Social Security.

- Read legal notices: especially anything involving a court case or account restraint.

- Don't assume every debt is private: tax debt and support obligations follow different rules.

- Treat your SSDI deposit as protected income: not as money that should flow through multiple mixed accounts without a paper trail.

What works and what doesn't

A good rule of thumb is to ask one question first. Is this a private consumer debt or a government or court-ordered obligation?

What usually works in your favor:

| Situation | Likely result |

|---|---|

| Medical debt from treatment | SSDI itself is generally protected from private garnishment |

| Credit card judgment | SSDI itself remains protected |

| Personal loan collection | Collector usually can't garnish the benefit payment itself |

| Pressure from debt buyers | Strong federal protection still applies to SSDI |

What doesn't work:

- Panicking over every collector letter

- Assuming a lawsuit automatically means your check will disappear

- Believing a collector's phone statement without checking the type of debt

- Ignoring the difference between SSDI and the bank account where it lands

If your debts are mostly medical, credit card, or consumer accounts, you may be in a safer position than you think.

When Creditors Can Pierce the SSDI Shield

The shield around SSDI is real, but it isn't absolute. Certain debts sit in a different legal category. These aren't routine consumer claims. They're obligations the federal government or a court can enforce directly.

As AARP explains, SSDI benefits can be garnished for specific federal debts and court-ordered obligations. The IRS can levy up to 15% for back taxes, defaulted federal student loans can be garnished up to 15% while leaving at least $750 monthly, and child support or alimony can lead to garnishment of 50-65% of benefits.

Federal tax debt

IRS debt is one of the clearest exceptions. If you owe back taxes, the federal government can levy part of your SSDI. The cap is up to 15% of each monthly payment.

For someone already budgeting every prescription, copay, and tank of gas, even that reduction can hurt. But it's different from a private collector draining the entire check. The law sets a limit.

This is one reason older claimants with physical disabilities need to take tax notices seriously. Many people fell behind not because they were careless, but because illness interrupted work, recordkeeping, or estimated payments. A person dealing with heart disease or cancer treatment may have let taxes slide because survival came first.

Defaulted federal student loans

This surprises many people in their 50s and 60s. Old federal student loans don't necessarily disappear with age. If they're in default, SSDI can be garnished up to 15%, but your benefit can't be reduced below $750 per month.

That floor matters. It doesn't solve the problem, but it creates a basic income safeguard.

For older disability claimants, these are often stale debts from decades ago. Some borrowed for their own schooling. Others borrowed to retrain after injury or job loss. The debt may have gone quiet for years, then resurfaced after benefits begin.

Old debt can feel dormant, but federal debt often stays legally alive much longer than private debt people assumed was gone.

The practical trade-off is this. Federal student loan garnishment is more limited than family support garnishment, but more dangerous than ordinary private debt because the government has direct collection tools.

Child support and alimony

Family support obligations are treated very differently from medical bills or credit cards. If there is a valid support order, SSDI can be garnished at much higher levels. The range cited above is 50-65%.

Not sure if you qualify?

Get a free case review from a New England disability team. You only pay if we win.

Call (617) 683-1983That is a severe hit to a monthly check. For many disabled workers, it can turn an already tight budget into a crisis. But courts and federal law place support obligations in a protected category because another person, often a child, is legally dependent on those payments.

If this is your situation, don't guess. The details matter. Support arrears, current support, and the specific order all affect how the withholding is handled.

What about Social Security overpayments

Another category older claimants should watch closely is overpayment. Sometimes Social Security says a person received more than they should have. That can happen because of reporting issues, work activity questions, or agency error.

The key point is simple. This is not the same as a private creditor trying to collect a debt. If the government claims an overpayment, the issue has to be addressed directly and quickly. Ignoring those notices usually makes things worse.

A simple way to sort the risk

If you're staring at a letter and trying to decide whether it's a real threat to your SSDI, use this quick sorting guide:

| Type of debt | Can it reach SSDI benefits |

|---|---|

| Credit cards | Generally no |

| Medical bills | Generally no |

| Personal loans | Generally no |

| IRS back taxes | Yes, within the legal cap |

| Defaulted federal student loans | Yes, within the legal cap and monthly floor |

| Child support or alimony | Yes, often at much higher levels |

| Social Security overpayment | Can affect benefits and must be addressed directly |

What works versus what backfires

The people most at risk are often the ones who avoid opening mail because they're overwhelmed. That's understandable, especially when pain, fatigue, and medication are part of daily life. But avoidance works badly when the debt is federal or tied to a support order.

These responses usually help:

- Responding early to tax or support notices

- Keeping copies of all agency letters

- Checking whether the debt is federal, private, or court-ordered

- Getting advice before agreeing to any payment you can't sustain

These responses usually backfire:

- Assuming all collectors have the same legal power

- Throwing away government notices with ordinary collection mail

- Relying on a phone representative's summary instead of the written notice

- Waiting until your deposit is smaller to investigate

If you're asking can ssdi be garnished, the honest answer is yes, but only in specific categories. Knowing those categories is what turns fear into a plan.

How Garnishment Works at Your Bank Account

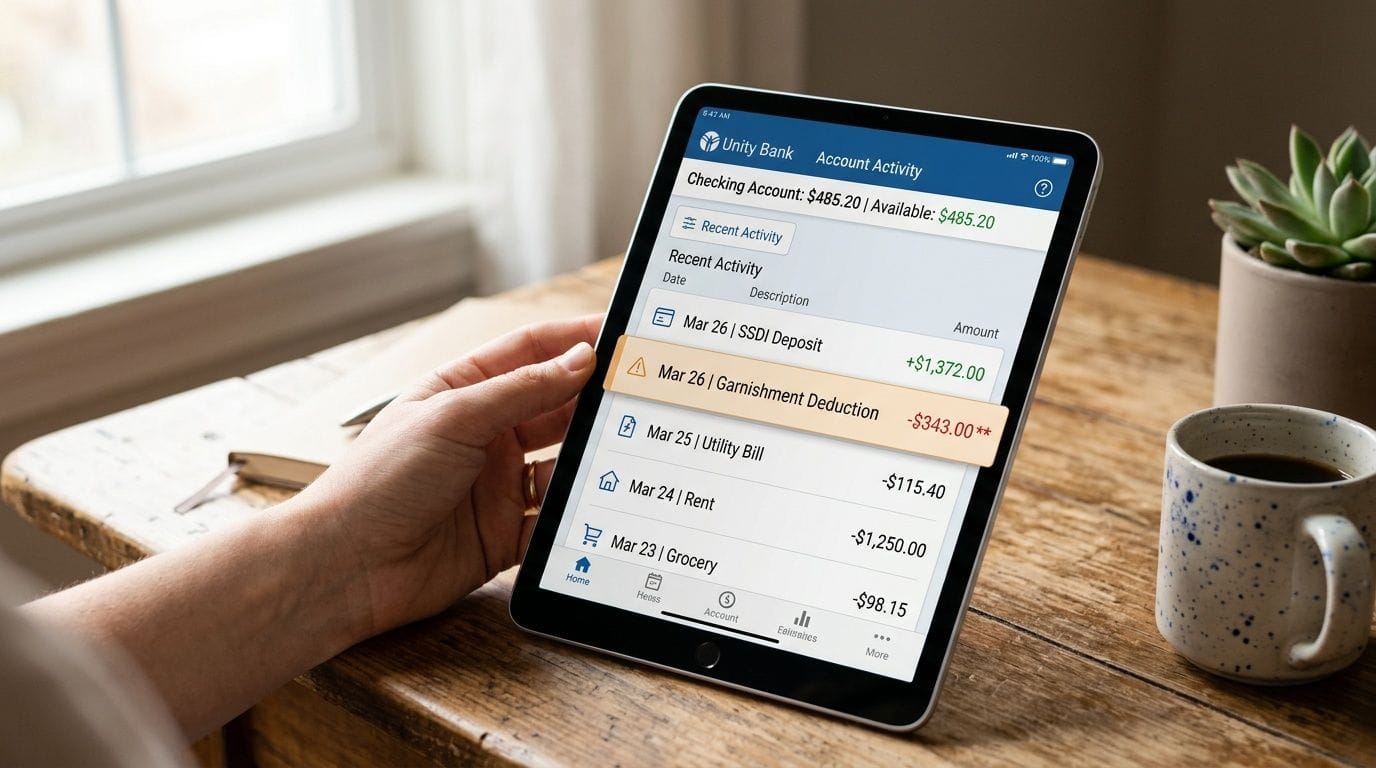

For many people, the most confusing part isn't the debt itself. It's what happens after the money hits the bank. That's where a lot of unnecessary panic starts.

When a creditor targets a bank account, the bank must perform a two-month lookback. It reviews the prior two months of deposits, identifies direct Social Security deposits, and automatically protects an amount equal to two months of those benefits. Funds above that amount may be vulnerable, especially if they're commingled with non-benefit money.

The two-month lookback in plain English

Think of the bank as checking two grocery bags at the door. One bag clearly belongs to Social Security. The other bag contains mixed items from different places. The bank can easily protect what it can clearly identify as SSDI from the recent deposit history.

The rule is concrete. If your monthly SSDI benefit is $1,000, the bank must protect $2,000 in the account under the two-month review rule described in the source above. If your monthly SSDI benefit is $1,500, the bank must protect $3,000.

That automatic protection is important because it doesn't depend on you racing to court before the bank acts.

Why commingling creates trouble

Commingling means mixing SSDI deposits with other money in the same account. That could be a spouse's paycheck, cash deposits, gig income, retirement withdrawals, or transfers from another account.

Older claimants often run into problems without realizing it. A household may be trying to simplify finances by putting everything in one checking account. From a daily budgeting perspective, that feels practical. From a garnishment-protection perspective, it can create a mess.

Keep your SSDI in its own lane. Separate accounts make it easier for the bank, the court, and your lawyer to prove what should be protected.

A dedicated account for direct SSDI deposits is usually the cleanest setup. It creates a clear paper trail and reduces the chance that protected money gets tangled up with unprotected funds.

What to do at the banking level

If you rely on SSDI as core income, these habits help:

- Use one account just for SSDI deposits: no side income, no shared payroll deposits, no random transfers if you can avoid them.

- Leave the direct deposit trail visible: direct deposit records matter because the bank is looking for identifiable Social Security deposits.

- Review statements every month: not casually, but line by line.

- Save notices from the bank: especially anything about a restraint, levy, or legal order.

Here is the practical difference:

| Banking choice | Why it matters |

|---|---|

| Dedicated SSDI-only account | Easiest way to show funds are protected |

| Mixed household account | Harder to trace protected deposits |

| Direct deposit maintained consistently | Helps trigger automatic protection |

| Frequent cash movement between accounts | Can complicate proof |

What many people misunderstand

People often assume one of two things, and both can cause trouble.

First, they assume protected benefits mean every dollar in the account is untouchable forever. That's not how the bank review works.

Second, they assume that if a bank freezes money, the protection must have failed completely. Sometimes the issue is identification, timing, or account mixing, not the loss of the underlying legal protection.

Worried a misstep could cost you benefits?

A short, free consultation now can prevent an expensive mistake later. No upfront fees.

Call (617) 683-1983If your account contains SSDI, the right question isn't only whether a creditor served the bank. The right question is whether the bank correctly identified and protected the SSDI funds it was required to protect.

Real Life Garnishment Scenarios for Claimants Over 50

Rules make more sense when they sound like real life. People between 50 and 64 usually aren't dealing with debt in the abstract. They're dealing with debt while limping through the grocery store, recovering from surgery, managing infusions, or trying to pace a day around pain and fatigue.

The former laborer with degenerative disc disease

A man in his late 50s spent decades doing heavy work. Now he has degenerative disc disease, chronic neck pain, and numbness that runs into one arm. He gets SSDI and starts receiving letters from a hospital collection department after imaging, injections, and physical therapy left him with large balances.

He's frightened because the letters mention legal action. He assumes that means the collector can take his monthly disability check.

In that situation, the key point is this. Medical debt is usually private debt. That means the collector may pressure him, and may even sue, but the SSDI benefit itself has strong protection against private garnishment. The practical priority is to keep the benefit deposit identifiable and not let fear push him into unaffordable payment promises.

The heart patient with old IRS debt

A worker in his early 60s leaves the workforce after a serious heart condition makes full-time employment unrealistic. He finally gets on SSDI. Then he receives notice about old federal tax debt from years when his work was irregular and records fell apart.

This is different from the hospital-bill situation. Tax debt falls into one of the limited categories that can reach SSDI. So his response can't be denial or delay. He needs to read every notice carefully, confirm what agency is collecting, and address the tax issue directly.

What often helps in cases like this is emotional reframing. The question isn't "Are all my benefits gone?" Usually, it is "What is the legal limit, and how do I stop this from becoming more disruptive than it has to be?"

The cancer survivor with defaulted federal student loans

A woman in her mid-50s fought cancer, left work, and now relies on SSDI while dealing with follow-up care and fatigue. She also has old federal student loans from a training program she once hoped would help her move into less physical work.

She thought those loans had faded into the background. Then a federal notice appears. This scenario feels especially cruel because the debt is old and the health crisis is current. But old federal student loans can still create garnishment risk.

The practical issue here is not only the legal rule. It's bandwidth. People in this stage of life are often juggling specialists, medication schedules, insurance paperwork, and family responsibilities. Debt notices get dropped in a pile because there are too many urgent things. That's understandable, but it allows federal collection problems to harden.

A debt letter means one thing. A federal debt notice means something else. Treat them differently.

The divorced claimant with chronic knee and back problems

A person in their early 60s with severe knee deterioration and lumbar pain starts SSDI after years of trying to keep working. There is also an older child support order with arrears.

Many people are often blindsided. They know private debt collectors are aggressive, so they focus on credit cards and medical debt. Meanwhile, a support order can have far more direct effect on the benefit check.

The lesson in this scenario is blunt but useful. Don't measure risk by how scary the letter sounds. Measure it by the legal category the debt falls into.

What these scenarios have in common

Different condition, different debt, same core problem. People are exhausted and trying to tell which threats are real.

A practical triage list helps:

- Private medical or consumer debt: usually frightening, often less dangerous to the SSDI check itself

- Federal tax debt: less common, more serious

- Federal student loan default: often old, still important

- Child support or alimony: highest urgency because withholding can be significant

For older claimants, clarity matters more than optimism. Once you know which bucket the debt belongs in, your next move becomes much easier.

Steps to Take If Your Benefits Are Wrongfully Garnished

A wrongful freeze or garnishment can make anyone panic. If you're already living with pain, weakness, limited mobility, or the fatigue that comes with cancer or cardiac disease, that panic hits even harder. The answer is to move in order, not all at once.

Start with the bank

Call the bank immediately and ask specific questions. Was there a levy, a garnishment order, or an account restraint? Which creditor or agency sent it? What amount was frozen? Did the bank identify direct Social Security deposits in its review?

Ask for copies of any notice the bank sent or received. You want names, dates, and the exact reason the account was restricted.

Want a straight answer about your claim?

Free consultation with an experienced SSDI team. No fees unless you win.

Call (617) 683-1983Gather proof fast

Don't rely on memory. Pull documents.

The most useful records usually include:

- Recent bank statements: especially statements showing direct Social Security deposits

- Your SSA benefit verification materials: anything confirming the benefit source

- The garnishment or levy notice: from the bank, creditor, court, or agency

- A timeline of deposits and withdrawals: simple, handwritten is fine if it's accurate

If your SSDI was paid into a separate account, your proof is usually cleaner. If the account was mixed, gather enough records to trace the protected deposits.

Challenge the freeze or garnishment

If protected SSDI funds were frozen or seized improperly, you may need to file a claim of exemption in court or use the bank's process to contest the restraint. The exact procedure depends on who initiated the action and how the funds were handled.

In such situations, speed matters. Delay can turn a fixable mistake into a cash-flow emergency.

Protected money still has to be defended when a bank or creditor gets it wrong.

Don't overlook larger relief options

Sometimes the garnishment problem is part of a broader debt crisis. In that situation, a narrow fix isn't enough. You may need a more thorough legal strategy.

According to SSA guidance discussing Chapter 13 bankruptcy relief, filing Chapter 13 triggers an automatic stay under 11 U.S.C. § 362 that instantly halts creditor actions, including federal tax levies and other garnishments, and it can place debts like back taxes or child support into a 3-5 year repayment plan while preserving full SSDI benefits during the process.

That doesn't mean bankruptcy is right for everyone. It means serious garnishment problems sometimes need a serious tool.

A short emergency checklist

When your account is frozen, use this order:

- Confirm the source with the bank.

- Get the paperwork before details disappear into phone confusion.

- Identify the debt category so you know whether the garnishment was even legally possible.

- Assert the exemption quickly if protected SSDI funds were touched.

- Get legal help if the amount frozen threatens rent, food, medication, or utilities.

People often lose time by arguing emotionally with a collector. Documentation and procedure usually matter more than the phone call.

How We Help Protect Your SSDI Income

People in their 50s and early 60s often come to this issue from two directions at once. First, they're trying to win SSDI because a physical condition has pushed them out of work. Second, they're trying to protect whatever income they have left from collection pressure. Those problems overlap more than anticipated.

A strong disability case helps at the front end. If you're suffering from degenerative disc disease, severe knee problems, orthopedic injuries, neck disorders, neurological disease, cancer, or heart conditions, the right record development and hearing preparation matter. The monthly benefit you're fighting for is too important to leave to guesswork.

Protection matters on the back end too. Even when SSDI has a strong federal shield, mistakes still happen. Banks freeze accounts. Creditors overreach. Government notices get misunderstood. Support and tax issues require careful handling. What looks like a simple garnishment question often turns into a records question, a procedural question, or a strategy question.

Experienced SSDI representation makes a difference. A firm that understands disability law, administrative hearings, and the practical realities of fixed-income living can do more than file forms. It can help spot which debt threats are real, which ones are bluster, and what steps protect the benefit once it starts coming in.

For many claimants, especially those with physical impairments that worsen with stress, the best legal help does two things at once. It builds the strongest possible disability claim and helps protect the income that claim is meant to provide.

If you're worried about whether can ssdi be garnished in your situation, don't settle for a generic answer. The right answer depends on the type of debt, the source of the collection action, the way your bank account is structured, and where your disability claim stands right now.

If you're applying for SSDI, appealing a denial, or dealing with threats to the benefits you depend on, Melanson Law Group can help you protect your rights and build the strongest case possible. Their team focuses on SSDI claims and appeals, with hands-on guidance for people whose medical conditions have taken them out of the workforce.