When people first look into disability benefits, the two acronyms they see everywhere are SSI and SSDI. It's easy to get them confused, but the difference comes down to one simple question: did you pay into the Social Security system through work?

SSI vs SSDI The Core Difference Explained

Both programs are run by the Social Security Administration (SSA) and provide critical financial support to people with disabilities. However, they serve entirely different populations based on completely different rules. Getting this distinction right is the first step toward a successful claim.

SSDI The Earned Insurance Program

Think of Social Security Disability Insurance (SSDI) like an insurance policy you've earned. As you worked and paid FICA taxes, you were accumulating "work credits." These credits are like the premiums you paid on your policy.

If you become disabled and can no longer work, you can file a claim on that insurance. Your eligibility is based on those work credits, not your current financial situation. You can have savings, own a home, and have other assets without it affecting your ability to get SSDI.

SSI The Needs-Based Safety Net

On the other hand, Supplemental Security Income (SSI) is a safety net program funded by general tax revenues, not Social Security taxes. It's designed to help disabled individuals who have very limited income and almost no resources to meet their basic needs for food and shelter.

To qualify for SSI, you must meet strict financial limits. The SSA looks closely at your income, your bank accounts, and even "in-kind" help you might get, like free rent from a family member. It’s for those who either don't have enough work credits for SSDI or who are in significant financial need.

Key Takeaway: The primary difference between SSI and SSDI is how you qualify. SSDI is for workers who 'paid in' through taxes, while SSI is for individuals with proven financial need, regardless of work history.

To make this even clearer, this table breaks down the fundamental differences at a glance.

At a Glance Comparing SSI and SSDI

| Factor | Social Security Disability Insurance (SSDI) | Supplemental Security Income (SSI) |

|---|---|---|

| Funding Source | Social Security trust funds (FICA taxes) | General U.S. Treasury funds |

| Primary Requirement | Sufficient work credits from past employment | Limited income and resources |

| Asset Limits | No limit on assets or unearned income | Strict limits (e.g., $2,000 for an individual) |

| Benefit Calculation | Based on your average lifetime earnings | A set federal rate, reduced by countable income |

| Healthcare | Medicare after a 24-month waiting period | Medicaid eligibility in most states, often immediate |

Understanding these distinctions is essential, as it determines not only your eligibility but also your benefit amount and the type of healthcare coverage you may receive.

Who Qualifies for SSI and SSDI?

While both SSI and SSDI are for people who can't work due to a medical condition, how you qualify for them is completely different. It's one of the biggest points of confusion for applicants, and getting it wrong from the start can lead to denied claims and lost time.

The single most important thing to understand is this: SSDI is an earned benefit, while SSI is a needs-based program. Think of SSDI like an insurance policy you paid into through taxes on your paychecks. SSI, on the other hand, is a safety net funded by general taxes for those with very limited income and resources.

Which path you take depends entirely on your personal history.

SSDI Eligibility: The Work Credit System

To be eligible for Social Security Disability Insurance (SSDI), you need to have a long enough recent work history. The Social Security Administration (SSA) measures this using a work credit system. You earn these credits by working and paying FICA (Social Security) taxes.

For 2026, you get one work credit for every $1,730 you earn, up to a maximum of four credits per year.

The number of credits you need depends on your age when you became disabled. Most people need 40 credits total, with 20 of those earned in the 10 years right before their disability began. This is called the "recent work" test.

But the SSA has special rules for younger workers who haven't had as much time to build a work history:

- Before age 24: You can qualify with just 6 credits earned in the 3-year period before your disability started.

- Ages 24 to 31: You may qualify if you have credits for working at least half the time between age 21 and the date you became disabled.

- Age 31 or older: You typically need the standard 20 credits in the 10 years before your disability.

Real-World Example: A 55-year-old mechanic who worked his whole life will easily have more than the 40 required credits. But what about a 28-year-old graphic designer who becomes disabled after working for only four years? She may still qualify for SSDI if she earned at least 14 credits (representing half the time between age 21 and 28).

SSI Eligibility: The Strict Financial Rules

Supplemental Security Income (SSI) works on a completely different set of rules. Your work history and work credits don't matter at all. What matters is your financial situation—right now.

Because SSI is a needs-based program, the SSA has very strict limits on your income and resources (the things you own).

Resource Limits for 2026

Resources are things like cash, money in bank accounts, stocks, and property other than the home you live in.

- An individual cannot have more than $2,000 in countable resources.

- A couple cannot have more than $3,000 in countable resources.

The SSA doesn't count everything. For example, the house you live in and one car are usually exempt. But anything beyond these basic exemptions is heavily scrutinized.

Income Limits for 2026

There are also strict limits on how much income you can have each month. This includes money you earn from a job as well as "unearned" income like gifts, unemployment, or pensions.

A critical concept unique to SSI is called "in-kind support and maintenance" (ISM). If a friend or family member helps pay for your rent, mortgage, or food, the SSA can count the value of that help as income. This will directly reduce your monthly SSI payment, a rule that does not apply to SSDI.

These two programs were born from different philosophies. SSDI was created to protect workers who contributed to the system, which is why it demands a solid work history. In contrast, SSI was designed as a safety net for the most financially vulnerable, which is why it scrutinizes income and resources, even counting help from family as income. These rules have been shaped over decades; for example, 1977 amendments reduced how much younger workers could receive from SSDI. As a National Academies Press report noted, by 2014, only 9% of people left the disability rolls due to medical recovery, showing just how difficult it is to return to work. Understanding these disability program dynamics and their historical context is key to navigating their complexities.

Understanding Benefit Payments and Financial Rules

Once you know which program you might qualify for, the next question is always about the bottom line: how much money will you actually receive each month? The way payments are calculated is one of the biggest differences between SSDI and SSI, and it directly shapes your financial reality.

One program is based on what you’ve earned, while the other is based on your current financial need. Getting a handle on these different financial rules is absolutely essential for planning your future.

How SSDI Calculates Your Monthly Benefit

Think of Social Security Disability Insurance (SSDI) as an insurance program you’ve been paying for with every paycheck through FICA taxes. Because of this, your benefit amount is tied directly to your work history and how much you earned over your lifetime.

The Social Security Administration calculates this using a formula based on your average indexed monthly earnings (AIME). In plain English, the more you earned and paid in Social Security taxes, the higher your monthly SSDI payment will be. It's a personalized amount, not a flat rate.

For 2026, the average SSDI payment is projected to be around $1,580 per month. However, this can vary a lot. Someone with a long history of high earnings could receive up to the maximum of $4,018 per month.

This is the single most important financial difference: SSDI has no resource or asset limits. You can have savings, own a home, have a second car, or hold other assets without it impacting your eligibility.

This is what makes SSDI a true insurance benefit. It was designed to replace lost income from work, not to force you to spend down your life's savings just to get the help you've already earned.

How SSI Determines Your Monthly Benefit

Supplemental Security Income (SSI) operates from a completely different starting point. Your payment isn’t based on your past work but on a standard federal amount designed to meet basic needs.

This is called the Federal Benefit Rate (FBR). For 2026, the FBR is expected to be $967 for an individual and $1,450 for a married couple. Keep in mind, this is the maximum amount you can receive.

Your actual monthly payment is almost always reduced by what the SSA considers countable income. This can be confusing, but it includes more than just a paycheck.

- Earned Income: Wages from any part-time work.

- Unearned Income: Things like unemployment, pensions, or even cash support from family and friends.

- In-Kind Support: The value of free room and board you might get from living with someone else.

If you have $100 in countable income for the month, your SSI check will be reduced by that amount. An individual who would normally get the maximum $967 would instead receive $867 for that month.

Comparing Payment Structures at a Glance

The financial rules for SSDI and SSI are polar opposites. One is an earned benefit that functions like insurance, and the other is a needs-based safety net. This table breaks down the core financial differences.

| Financial Rule | Social Security Disability Insurance (SSDI) | Supplemental Security Income (SSI) |

|---|---|---|

| Basis of Payment | Based on your average lifetime earnings. | A flat rate set by the government (FBR). |

| Asset/Resource Limit | None. There is no limit on savings or assets. | Strict limits: $2,000 for one person, $3,000 for a couple. |

| Impact of Other Income | Only earned income is limited by SGA rules. Unearned income (from savings, investments, etc.) does not affect benefits. | Nearly all types of income—earned, unearned, and in-kind—reduce your monthly payment after small initial exclusions. |

That "no asset limit" rule for SSDI is a lifeline for so many hardworking people. If you're a teacher, a construction worker, or an office manager who built up a nest egg, you shouldn't have to drain your savings to qualify for the disability benefits you paid for. Understanding this distinction is the key to protecting the financial future you worked so hard to build.

Navigating Healthcare with Medicare and Medicaid

The disability benefits you receive are only half the story. The other critical piece of the puzzle is healthcare coverage, and how you get it depends entirely on which program—SSDI or SSI—you qualify for.

These two healthcare paths are not the same, and the timelines are completely different. Understanding this is essential for planning how you’ll cover everything from doctor visits to the prescriptions you rely on.

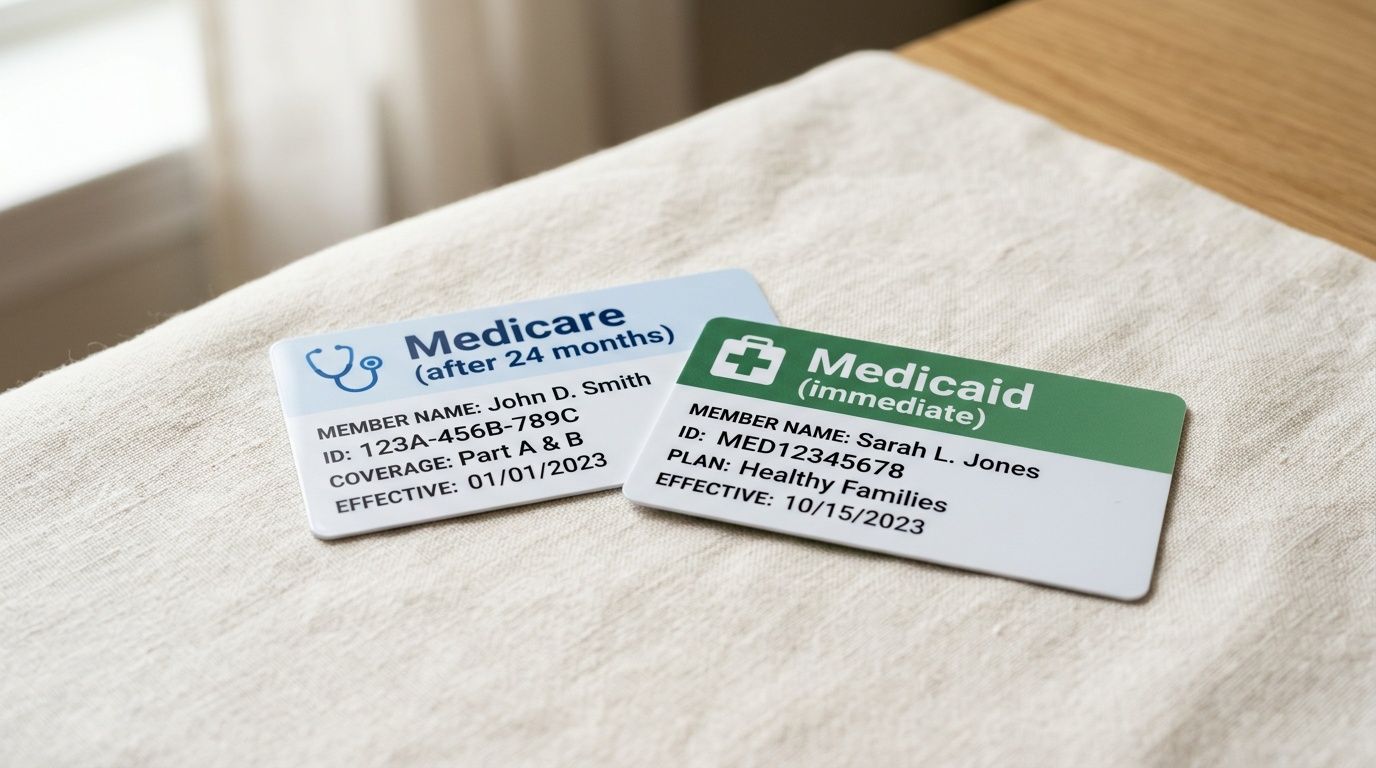

Medicare Coverage for SSDI Recipients

If you’re approved for Social Security Disability Insurance (SSDI), you will qualify for Medicare. But here's the catch most people don't see coming: the coverage isn't immediate. There’s a mandatory 24-month waiting period that starts from the date you're entitled to your first SSDI cash payment.

That two-year gap can be a major hurdle. It means that for two full years, you are responsible for finding your own health insurance, whether through COBRA, a spouse's plan, or a marketplace plan. This is a tough spot to be in when you’re already managing a disability.

Once that waiting period is over, you’ll be automatically enrolled in:

- Medicare Part A (Hospital Insurance): This is your coverage for inpatient hospital stays, care in a skilled nursing facility, hospice, and home health services.

- Medicare Part B (Medical Insurance): This covers your doctor appointments, outpatient care, durable medical equipment, and a wide range of preventive care.

You’ll also have the option to sign up for Medicare Part D (Prescription Drug Coverage), which is crucial for anyone managing a chronic condition with regular medications.

Medicaid Coverage for SSI Recipients

The path to healthcare is much more direct for those who qualify for Supplemental Security Income (SSI). In the vast majority of states, being approved for SSI means you are immediately eligible for Medicaid.

There is no two-year wait. This immediate access is a lifeline for people with urgent medical needs who have very limited income and resources. Medicaid often provides more extensive benefits than Medicare, sometimes covering services like long-term nursing care that Medicare doesn’t.

For a healthcare professional referring a patient sidelined by chronic illness, clarifying the difference between SSDI and SSI is essential to prevent application pitfalls. SSDI is an insurance program for those with enough work credits and no asset limits, whereas SSI is a welfare program for those with under $2,000 in resources. Understanding these distinctions, and how firms like Melanson Law Group can build a case, is key. You can find more data on the disability insurance program from the Urban Institute.

When You Qualify for Both: Dual Eligibility

What happens if your situation puts you somewhere in the middle? Some people are eligible for both SSDI and SSI at the same time, which is known as having “concurrent benefits.” This is common when a person has enough work history for SSDI, but their monthly disability payment is very low.

If your SSDI payment is less than the federal SSI income limit, you may be able to get an SSI payment to make up the difference. This "dual eligibility" is a powerful combination that offers the best of both worlds:

- Immediate Medicaid: You get access to comprehensive healthcare right away through your SSI eligibility.

- Future Medicare: You still get Medicare after the 24-month SSDI waiting period is over.

This ensures you have continuous health coverage while you wait for your Medicare benefits to kick in. It’s a perfect example of why it’s so important to apply for both programs if there’s any chance you might qualify.

The Application and Appeals Process

Applying for SSI or SSDI can feel like you’re stepping into a bureaucratic maze. Whether you apply for one program or both, the path to getting approved is rarely simple or quick. It demands a lot of patience, and frankly, it can be discouraging when you run into the high initial denial rates.

But knowing the map of that maze is the first step to finding your way through it. The process is almost the same for both SSI and SSDI, and understanding what to expect at each turn can keep you from making mistakes that cause delays or, worse, a final denial.

The Four Key Stages of a Disability Claim

Your disability claim will go through a few layers of review. Each one is a new chance to get an approval, and it’s critical to treat every stage seriously.

Initial Application: This is where it all starts. You’ll submit your application online, over the phone, or in person, along with all the medical records and work history you can gather. The Social Security Administration (SSA) will first check if you meet the basic technical rules, then pass your file to a state agency to decide if you meet the medical ones.

Reconsideration: If your initial application is denied—which is incredibly common—your first appeal is called Reconsideration. A new claims examiner, who had nothing to do with the first decision, is supposed to take a fresh look at your entire file, including any new medical evidence you’ve submitted.

Administrative Law Judge (ALJ) Hearing: If the Reconsideration is also denied, you can request a hearing with an Administrative Law Judge (ALJ). This is a game-changer and often your best shot at winning. It’s a real hearing where you or your lawyer can explain your case directly to the judge who will decide it.

Further Appeals: If the ALJ says no, you still have options, but they get much more technical. You can ask the Appeals Council to review the judge’s decision and, if that fails, you can file a lawsuit in Federal Court. These later stages are very complex and almost always require an experienced attorney.

Why Persistence Is Your Greatest Asset

The initial denial letter is where most people get discouraged and just give up. That’s completely understandable, but it’s also a huge mistake. Initial denial rates for disability claims are consistently around 65-70%. A denial is more the rule than the exception.

The most important thing to remember is that an initial denial is not the end of the road. It's a standard part of a long process. The Administrative Law Judge (ALJ) hearing is where a significant number of claims are finally approved, but you can only get there by appealing the first two denials.

Giving up is exactly what the system seems designed to make you do. But persisting is how people get the benefits they need. Think about this: as of December 2024, SSDI was paying benefits to over 8.6 million disabled people, with an average monthly benefit of $1,580.79. Those numbers represent millions who stuck with it. You can see these stats for yourself in the Social Security Administration's official reports.

The ALJ Hearing: Your Best Chance to Win

The ALJ hearing is completely different from the paper-shuffling of the first two stages. This is your chance to be seen as a person, not just a file number. You can speak directly to the judge, explain in your own words how your condition limits you, and answer their questions.

This is where having a skilled guide really pays off. An experienced attorney knows how to prepare you for the judge's questions, how to present your medical history as a compelling legal argument, and how to cross-examine the vocational or medical experts the SSA brings to the hearing.

A firm like Melanson Law Group, with a retired Social Security Judge like Jack Melanson who has decided over 6,000 of these claims, has seen it all from the other side of the bench. They know exactly what a judge needs to hear and see to approve a case. An expert lawyer will:

- Develop the Medical Evidence: They don't just file what you have; they work to get the right opinions from your doctors and make sure your file proves your limitations according to the SSA's rules.

- Prepare Your Testimony: They'll help you practice telling your story in a way that is clear, credible, and directly addresses the legal standards for disability.

- Challenge Unfavorable Testimony: When the SSA's vocational expert lists jobs they think you can do, your attorney will be ready to challenge them and show the judge why those jobs are not realistic for you.

Getting through this complex system isn't just about being disabled; it's about proving you are disabled according to the SSA’s very specific and often confusing rules. Having an expert on your side can be the one thing that makes the difference between another denial and finally securing the benefits you earned.

Choosing Your Path: SSI, SSDI, or Both

Knowing the rules for SSI and SSDI is one thing, but applying them to your own life is where things get real. The right choice isn’t always obvious. It hinges entirely on your work history, your financial situation, and the nature of your disability.

Making the right decision from the start can save you from months of frustrating delays. To help you figure it out, let’s walk through three common scenarios we see all the time. They show who should apply for which program—and, just as importantly, when you should apply for both.

Scenario 1: The Long-Term Worker

Think of a 50-year-old construction worker who’s been on the job since his early twenties. He now has a severe back injury that makes work impossible. He’s paid Social Security taxes with every paycheck for decades and has some savings tucked away.

- Best Path: Apply for SSDI only.

- Why: His long and consistent work history means he has more than enough work credits to qualify. Crucially, his savings and the home he owns won’t count against him, because SSDI has no asset limits. His benefit amount will be based on his lifetime earnings, reflecting his long career.

This is the classic SSDI candidate: someone whose ability to work was cut short by a disability after years of paying into the system.

Scenario 2: The Lifelong Disability

Now, picture a 30-year-old who has a condition that’s made it impossible to hold down a steady job. He has almost no work history, no significant savings, and lives with family members who help cover his expenses.

- Best Path: Apply for SSI.

- Why: Without a substantial work history, he simply won't have the credits needed for SSDI. SSI was designed for exactly this situation. It provides a financial safety net based on need, not on how much you’ve worked. He will also likely qualify for immediate Medicaid, which is critical for managing his health.

Scenario 3: The Low-Earning Worker

Finally, let’s look at a 42-year-old part-time retail worker who becomes disabled. She has worked just enough to qualify for a small SSDI payment, but the amount is very low—maybe only $600 per month. This is well below the federal benefit rate for SSI. She also has minimal savings, under the $2,000 resource limit.

- Best Path: Apply for both SSI and SSDI (this is called a "concurrent claim").

- Why: This is a strategic move to maximize her monthly support. She can receive her earned $600 SSDI payment, and then SSI can add to it, bringing her total monthly income closer to the full federal benefit rate.

Key Advantage: By filing a concurrent claim, she gets the best of both worlds. She gains immediate access to Medicaid through her SSI eligibility, which covers her healthcare needs during the long 24-month Medicare waiting period for SSDI.

Filing for both programs when you fall into this "in-between" category is often the smartest decision you can make. It ensures you get the highest possible monthly income and secures vital, continuous health coverage from day one.

The Social Security Administration will evaluate your eligibility for both programs when you apply, but knowing to pursue a concurrent claim can make a massive difference in your outcome. If you're unsure which path is right for you, a firm like Melanson Law Group can help you analyze your situation and build the strongest possible case.

Of course. Here is the rewritten section, adopting the specified human-written style, tone, and formatting.

Your Top Questions About SSI and SSDI Answered

Even after you understand the basic differences between SSI and SSDI, the practical side of applying for benefits can feel overwhelming. People often have the same key questions about the process. Let’s tackle some of the most common ones with straightforward answers.

How Long Does a Disability Claim Actually Take?

The honest answer? It takes a lot of patience. An initial decision on your application will typically take 3 to 6 months. If your claim is denied—which happens to most people the first time—and you file an appeal for Reconsideration, that step will add another 3 to 5 months to your wait.

If you have to go to the next level and request a hearing with an Administrative Law Judge (ALJ), you could be waiting for a hearing date for several months or even over a year, depending on the backlog in your area. Because these waits are so long, it's absolutely critical to file your appeals on time to keep your case moving.

Can I Work at All While Receiving Benefits?

Yes, you can, but the rules are extremely strict and you have to be careful. The Social Security Administration (SSA) actually has programs meant to encourage people to try returning to work, but it’s all based on your earnings.

The most important term to know is Substantial Gainful Activity (SGA). If you earn more than the monthly SGA limit, the SSA will almost always decide you are not disabled. For 2026, the SGA amount is projected to be over $1,620 a month for non-blind individuals.

The SSA also provides work incentives. For example, SSDI recipients get a Trial Work Period, which lets you test your ability to work for nine months without it affecting your benefits, no matter how much you earn during that time.

A Word of Caution: The rules for working are complicated and vary between SSI and SSDI. You are required to report every penny you earn and all work activity to the SSA. Failing to do so can lead to overpayments you have to pay back or a complete suspension of your benefits.

What Happens if My Condition Gets Better?

The SSA doesn't just approve you for benefits and forget about you. They conduct periodic reviews, known as Continuing Disability Reviews (CDRs), to determine if your medical condition has improved enough for you to be able to work again.

How often they check on you depends on how likely they think improvement is:

- If medical improvement is expected, they might review your case within 6 to 18 months.

- If improvement is considered possible, a review will likely happen every 3 years.

- If improvement is not expected, you’ll probably be reviewed every 5 to 7 years.

If the SSA decides your condition has medically improved and you can return to work, your benefits will stop. You do, however, have the right to appeal that decision and provide new evidence to prove you are still unable to work.

Knowing the difference between SSI and SSDI is just the first hurdle—getting through the actual process is a whole other challenge. The team at Melanson Law Group brings the expertise of a retired Social Security Judge and a seasoned litigator to help guide you at every stage.

To get the help you need, from filing your initial claim to representing you at a hearing, visit https://www.melansonlawgroup.com for a no-cost case evaluation.